Wondering how to save money when you have none? You’re not alone. Even in wealthy countries like Canada and the United States, millions of people face this challenge.

Unfortunately, personal finance writers often gloss over this scenario when discussing the benefits of saving. We often tell people it only takes $500 per month to become wealthy in the long run.

Well, what if you don’t have $50 to spare, let alone $500? This article is for you.

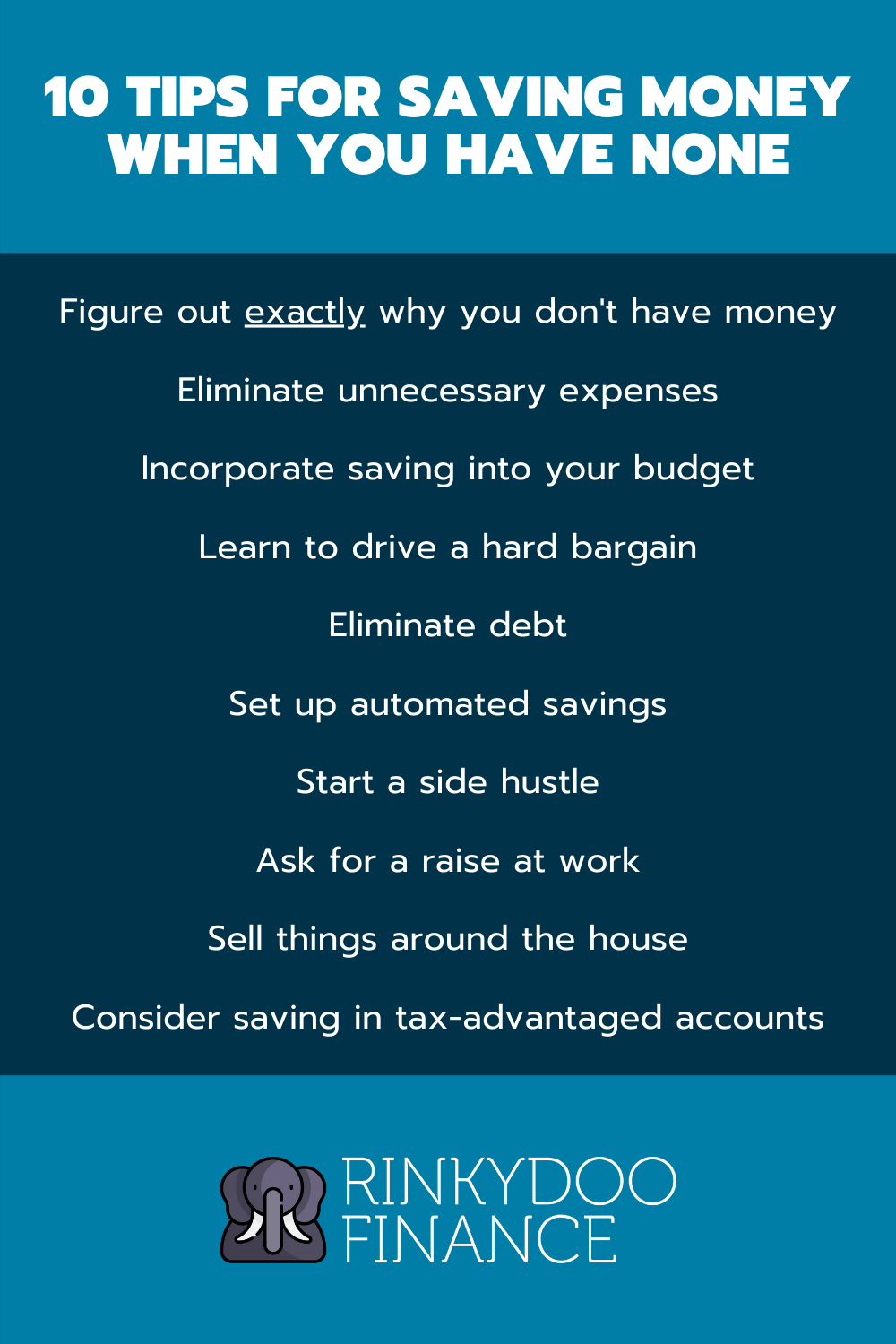

10 essential tips for saving money when you have none

1. Figure out exactly why you don’t have money to save

Often, people go through life knowing they have no money to save yet never digging into the underlying reasons. The end result is that they view being broke as a fundamental part of their identity.

Breaking out of this rut starts with figuring out why you don’t have money to save. For a list of common reasons, check out this article. Whatever your situation is, take note and begin seeing it as a problem to be solved.

Two things will likely happen once you do this.

First, you’ll begin seeing solutions everywhere, even when you’re not consciously looking for them. That’s how our brains work!

Second, you’ll be more likely to adopt productive attitudes about money, work, and value.

People often think these attitudes – which I list and discuss here – are only possible after you’ve obtained money. In reality, you need to adopt them first for any hope of climbing the wealth ladder without a substantial inheritance or a winning lottery ticket.

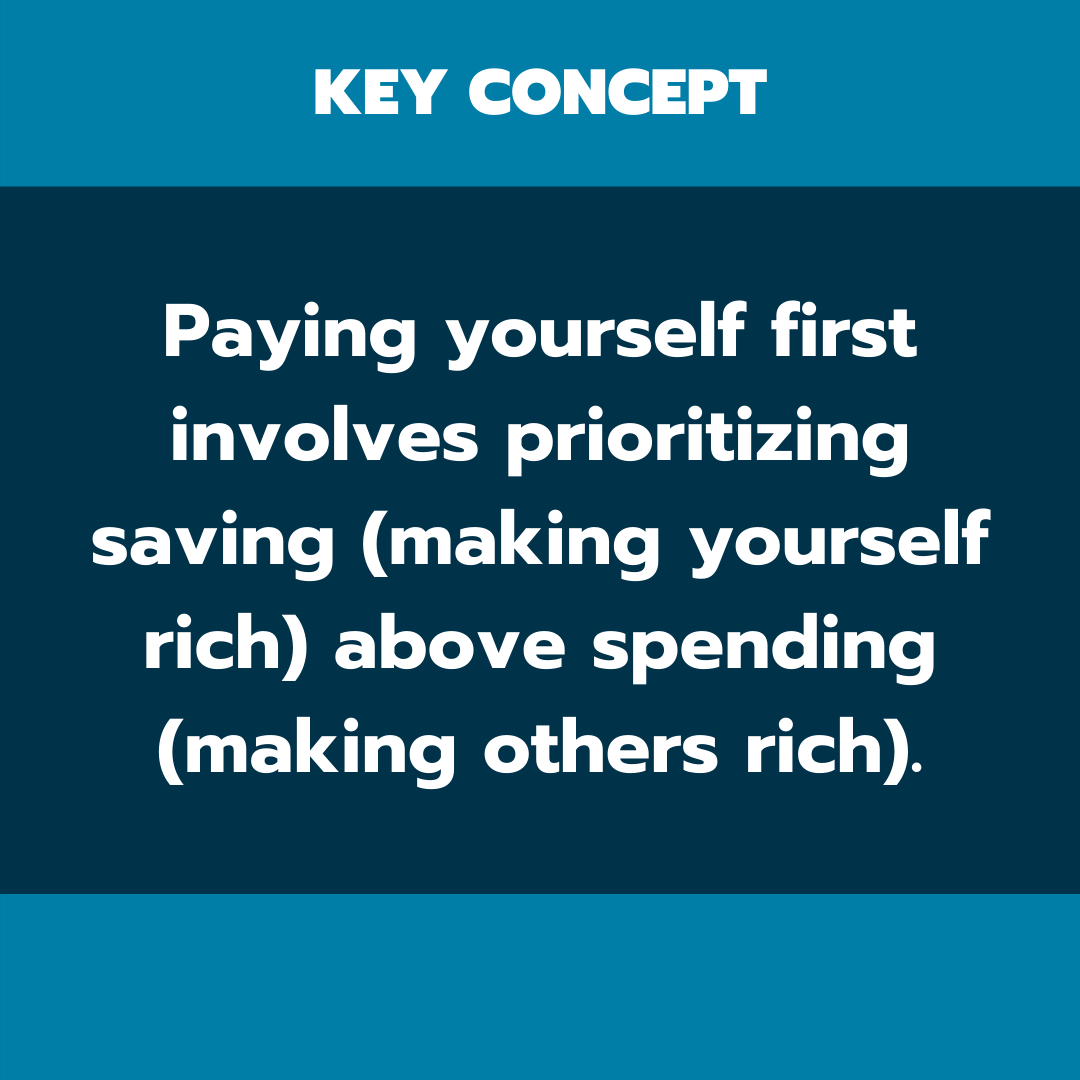

2. Eliminate unnecessary expenses and pay yourself first

Before you think about earning more, make sure to use your existing income as efficiently as possible. That means slashing unnecessary expenses and saving a portion of every paycheck.

In personal finance, we call this concept “paying yourself first.”

Many people do the exact opposite. Saving is the last thing they think about every month.

Instead, they prioritize bills and even completely discretionary purchases, only saving what’s left. The problem? What’s left usually isn’t much, if anything at all.

If you see yourself in what I’ve just described, it’s time for a change.

Common unnecessary expenses include:

- costlier internet, phone, and TV plans than your actual usage necessitates

- excessive food takeout

- impulse purchases at the grocery store

- unused subscriptions (i.e. gym memberships and Netflix)

These little items add up to hundreds, perhaps even thousands, of wasted dollars every year.

Of course, don’t ignore bigger money sinkholes either, such as:

- vehicle expenses exceeding 10% of your income

- housing expenses exceeding 32% of your income

After slashing these and other unnecessary expenses, you’ll likely find you actually do have money to save. It was just hiding.

Pro-tip

Not sure where to begin slashing?

Look through your bank statements for the past few months and identify expenses that don’t really improve your life or deliver substantial happiness.

You should be able to identify these now that you’re removed from the excitement accompanying any new purchase.

These will ultimately be some of the easiest expenses to slash since you really won’t miss them. As such, this is a great place to start!

3. Incorporate saving into your budget

Budgets aren’t just for expenses. They’re also extremely useful for setting savings targets.

This is tied very closely to the idea of paying yourself first. Saving needs to become an item in your budget no less important than bills and groceries. After all, your savings are all you’ll have to cover those items should your income ever cease.

Hopefully that helps you see the urgency of saving and pushes you into action.

Tips for incorporating saving into your budget

1. Set a clear target

Figure out how much you need to save on a monthly basis to achieve your goals. Some people target what’s known as a financial independence number.

While I’d recommend getting to that point, you may have humbler ambitions when first starting out. Even if you simply target $50 per month, it’s a start. You’ll have a target to work towards using the other tips in this article.

2. Reevaluate your target often

Periodically, you’ll need to reevaluate your budget, including your savings target. Specifically, ask yourself whether your capability to save has increased. If it has, increase the portion of your budget allocated towards saving.

3. Track saving as you would any other budget category

Tracking your budget is a crucial part of organizing your finances. Apps like Mint allow you to track both savings and expenses, creating a clear picture of your monthly cash flow.

Pro-tip

Even if you’re only able to set a savings target of $50 every month, it’s a start! Get in the habit of saving money and you’ll be surprised at how quickly your stash grows along with your motivation to keep pushing.

4. Learn to drive a hard bargain

You can only slash so many items from your budget before hitting a brick wall. This is especially true if your inability to save is rooted in something other than excessive discretionary spending.

Once you reach that point, it’s time to start negotiating. Many people don’t even realize this is an option. They think their bills are set in stone. In reality, there are very few expenses you can’t adjust in your favor through effective negotiation.

Bills to consider negotiating include:

- telecommunications (internet, phone, and cable)

- credit card interest

- insurance premiums

- routine car maintenance

- mortgage rates

By reducing even just one of these expenses, you can potentially save hundreds of dollars per month. That’s money you can use to save and invest.

Steps for negotiating your bills

Now, I’m not a natural haggler. If you’re in the same boat, negotiating your bills may seem daunting. We’re precisely the type of people who need to do this, though. Our aversion to price-related confrontation means we’re almost certainly overpaying for things.

Besides, negotiating really isn’t all that scary once you systematize it. In fact, with the correct strategy, you can remove the haggling component altogether.

Here are the steps I recommend.

1. Conduct market research

What are other companies charging for the product or service you’d like to trim? Often, you’ll find substantial incentives for new customers. Even if the monthly payments climb back to what you’re currently paying after the promotion is over, make note of these competing offers.

2. Call your current provider and, if applicable, explain your findings

If the numbers are on your side, this shouldn’t be a difficult conversation. The person you’ll be speaking to most likely understands basic math. If they want to keep you as a customer, which is almost always the case, they’ll need to start crunching numbers.

Even if they decline to do this, you win. Remember, you’ve got that competing offer you can claim.

But what if you weren’t able to find a better offer in the first step? All hope is not lost. You can still tell the person on the other end you’re not happy with their price and intend to keep looking.

Then, simply say, “so what can you do for me?”

This phrasing is important. Consider the alternative, “is there anything you can do for me?” This sets you up for a binary answer, which will almost certainly be negative.

Meanwhile, the question I’ve recommended is open-ended. It puts the customer service representative on the spot.

Often, this will be enough to get you a deal. If they won’t budge, keep looking out for better offers to present them next time you call. In the meantime, try negotiating other bills.

3. After you’ve negotiated one bill, capitalize on your momentum

Negotiating a bill down, particularly for the first time, is quite exhilarating. Use that momentum to your advantage. Go on a negotiation rampage, slashing as many bills as you can in one sitting.

Remember, when it comes to recurring expenses, it doesn’t take massive cuts to save. Even just $20 in savings per month adds up to $240 annually. That’s a step up from having $0 to save.

5. Eliminate debt

Debt, particularly the high-interest variety, severely impacts your ability to save money.

Think about it.

Until you eliminate debt, a portion of every paycheck belongs to someone else. That’s money you can’t save, invest, or otherwise use as you see fit.

Of course, provided you have the funds, you can certainly save while paying off debt. If you don’t have money to save because it’s all going towards monthly payments, though, that’s a different story.

Tips for eliminating debt so you can save more

Here are some tips for increasing your cash flow by eliminating debt, which will leave you with more money to save every single month.

1. Reduce your interest payments in the long run with the debt avalanche method

This method involves using any excess funds to make aggressive payments on whichever loan has the highest interest rate. Meanwhile, you’ll make the absolute minimum payments on everything else.

Once you’ve eliminated that debt, you’ll shift your attention to the loan with the second-highest interest rate, and so on.

The end result is that you’ll build momentum while also limiting the amount of interest you pay in the long run. Read more about the debt avalanche method on Investopedia.

2. Also consider the debt snowball method

The debt snowball method is also worth considering. It involves using excess funds to make aggressive repayments on whichever loan has the lowest balance. Everything else gets the bare minimum payment.

Now, under the right circumstances, a debt avalanche will save you more money.

However, the debt snowball method’s magic lies in its ability to generate momentum. By the time you start focusing on larger balances, you’ll have already eliminated numerous smaller debts. As such, you’ll likely have the confidence to keep going.

Choose whichever method gets you to the finish line and frees up more money to save sooner rather than later.

3. Don’t be afraid to eliminate low-interest debt, too

In personal finance circles, people often discourage the idea of rushing to eliminate low-interest debt such as car loans and mortgages. I understand this. In fact, I’m in no particular hurry to eliminate my car loan.

The key thing to note, however, is that this loan doesn’t limit my ability to save. I can make that $415 per month payment without skipping a beat.

If that weren’t the case, it would absolutely make sense to eliminate my car loan as quickly as possible, even though the interest rate is just 1.09%.

Keep this in mind when deciding which loans to get rid of.

4. Consider a debt consolidation loan

If you’re having trouble keeping up with monthly payments on numerous loans, consider debt consolidation. This type of loan provides a lump sum you can use to pay off multiple obligations, consolidating them into a single monthly payment.

In addition to being incredibly convenient, this method may also allow you to secure a lower interest rate. This is especially true if aspects of your financial situation – such as your credit score or income – have improved since you initially took on the smaller loans.

Many financial institutions offer debt consolidation loans, including traditional banks.

6. Set up automated savings

Relying on your own willpower to save money isn’t necessarily the best approach, particularly if you’ve had difficulty in the past. Many people swear by automation instead, having a certain amount of money funneled into savings on a regular basis.

I stick with $1,200 a month. This represents a specific percentage of my income. As I earn more, the dollar amount will increase in keeping with that percentage.

There are more creative ways to go about this as well. For example, consider round-up savings apps like Acorns and Moka. Whenever you make a purchase, these apps save the difference between the purchase amount and the nearest dollar.

For example, if you spend $4.50 at Starbucks every morning, a round-up savings app would invest 50 cents for you. You wouldn’t even miss the money on a daily basis but it would add up to $182.50 within a year. That’s just from one expense!

However you go about it, automating your savings can be an incredibly powerful strategy. I highly recommend it if you regularly find yourself tempted to spend rather than save.

Pro-tip

When automating your savings, make sure you keep a sizeable cash buffer in your account at all times. You don’t want withdrawals to push your account into overdraft, which would typically incur a fee.

This is actually an advantage of the automated savings strategy. After all, your buffer is a form of savings on its own.

7. Start a side hustle

There’s a reason I haven’t talked about increasing your income until now. Unless you manage money wisely, there’s no guarantee earning more of it will actually benefit you. Now that I’ve covered a few tips for getting your finances under control, though, let’s get that income up!

In my article on ways to earn money quickly, I list ideas such as:

- babysitting

- tutoring

- freelancing

- driving for Uber

- selling items on Etsy

These have the potential to be much more than quick cash grabs, though. Freelancing is a great example. Take it seriously enough and you could earn a substantial amount of money every month. If your day job covers your bills, all of that extra money should be free for saving.

Tips for earning money on the side

Here are some tips for maximizing your efficiency when it comes to side work.

1. Avoid get-rich-quick schemes like the plague

Side hustles involve work, plain and simple. They certainly won’t make you rich overnight. In fact, any side hustle promising quick riches is far more likely to cost you substantial amounts of money and time.

Stick with proven and legitimate side hustles such as the ones I listed above. Freelance writing is my personal favorite side hustle. On a website like Upwork, I can pump out a 1,000-word article in roughly an hour and earn $25.

Upwork also offers side work for web developers, graphic designers, and those in a whole host of other fields that lend themselves well to the gig economy.

2. Always aim to leverage your side hustle into something greater that occasional gig work

As much as I love freelancing, it can become a trap if you’re not careful. Most client relationships revolve around you building their streams of passive income while being underpaid. It’s just the nature of the game.

That’s why I’ve moved my side hustling in the direction of building a blog for myself. My experience writing for other people has earned me quite a bit of money. However, that money pales in comparison to the funds I could make building and monetizing my own blog.

This is the mindset I encourage all freelancers to adopt. Use the skills gleaned from your side hustle to eventually obtain something greater, such as a major project of your own or equity in a client’s platform.

3. Be mindful of taxes

Side income is not tax-free. Refer to your local tax laws and be sure to set enough money aside so you won’t be left scrambling when the bill comes due.

You should also keep taxation in mind when setting your prices. Charge enough to make it worth your while even after the government takes a chunk out of your earnings.

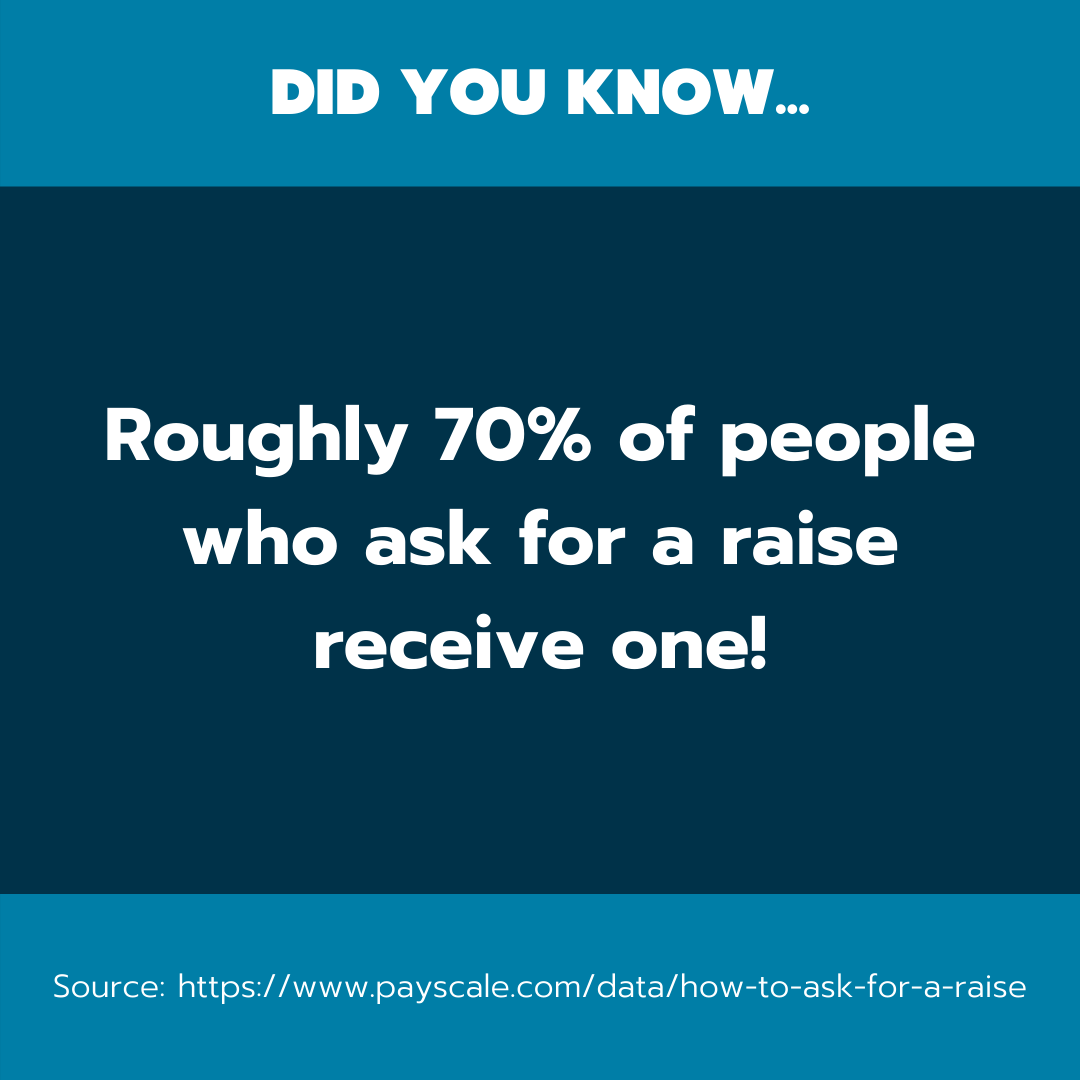

8. Ask for a raise at work

If you feel deserving of a raise, don’t be afraid to ask for one. You may even want to try this before picking up a side hustle. An affirmative answer could leave you with enough money to start saving.

The odds are in your favor, too. According to a study by Payscale, roughly 70% of people who request raises get them.

Tips for requesting a raise

Asking for a raise isn’t as scary as you might think, especially if you go about it the right way.

1. Do your research

It pays to do your research before requesting a raise. Figure out the typical salary range for someone with your level of experience using a site like Payscale.

If your salary falls short, use that information as leverage.

2. Gauge your current standing within the organization before requesting a raise

You never want to ask for a raise when people aren’t particularly thrilled with your performance. In other words, read the room. Your likelihood of receiving a raise will be much higher if you’ve been at the top of your game for several months.

3. Bring lots of evidence to build your case

Don’t count on your superiors being acutely aware of your stellar performance. You’d be wise to bring evidence. That includes concrete examples of how you’ve stepped up to the plate lately, perhaps by taking on greater responsibilities or delivering extraordinary results.

Organize this information into a readily-accessible format so you can highlight key points during the conversation.

4. Avoid ultimatums

Saying “give me a raise or I quit” is just a bad career move. Even if you somehow squeeze a raise out of this approach, you’ll lose in the long run. Your employer will question your loyalty to the company, costing you growth opportunities and perhaps even shortlisting you for termination.

Negotiate a raise on merit, not threats.

9. Sell things around the house

If you’ve never looked around your house for things to sell, I guarantee you’ve got money lying around in the form of old “junk.”

You’d be surprised what people are willing to buy on sites like eBay. I’ve sold broken watches, old guitars, and other items I assumed were worthless.

As the old saying goes, though, one man’s trash is another man’s treasure. Marketplaces like eBay open you up to millions of potential buyers.

Once you sell an item, take the proceeds and dump them straight into savings.

Pro-tip

Whenever you go shopping, start thinking about residual value rather than solely the price tag. Choose items you could potentially sell and recoup some of your money from once you’re done using them.

I used this logic when I went shopping for a new office chair. I chose a used Herman Miller Aeron because I know I could flip it relatively quickly and recoup most, if not all, of my money.

So while it cost me more upfront, I actually lose less in the long run than I would with a generic chair from Staples costing half as much.

10. Consider saving in tax-advantaged accounts

Some tax-advantaged accounts allow you to save money while also increasing your income.

Take the 401k in America or the Registered Retirement Savings Plan in Canada. The money you contribute to either of these accounts decreases your taxable income for the year. You’ll get a bigger tax refund, which may motivate you to save more aggressively.

The key caveat with tax-advantaged accounts is that they’re geared towards long-term savings. There are serious financial downsides to pulling money out of these accounts early. Work with a financial advisor to identify the best approach.

Habits to avoid when trying to save while you have no money

Now that I’ve given you plenty of tips for saving money while you have none, let’s look at things to avoid.

Procrastination

It’s very easy to tell yourself you’ll start saving once you’re making more money. While saving certainly gets easier as your income increases, you need to build productive habits as soon as possible.

After all, as I mentioned earlier, more money does not automatically come with good habits.

Racking up rewards points

While racking up rewards points may make you feel financially savvy, be very cautious. Hanging onto cash will always be more advantageous than spending it for the sake of accumulating points.

By all means, collect points on purchases you would’ve made anyways (i.e. gasoline or groceries). Just don’t get lured into a tap-happy craze in the process.

Falling for hyped-up sales

Participating in a sale is only financially advantageous if you needed to purchase the items in question anyway. Otherwise, you’re just losing money.

It sounds logical, right? Well, many people fall into this trap anyway because marketers are really good at convincing us we need something and then reeling us in with a discount. Don’t fall for it. Saving $10 on a pair of shoes you didn’t need is not the same as saving $10 in cash.

Lifestyle creep

Sooner or later, you’ll probably end up making more money. When that happens, avoid lifestyle creep, which is the habit of increasing your spending alongside your income.

Ideally, save or invest as much of your discretionary income as possible.

Conclusion

If you’ve been wondering how to save money when you have none, I hope this article has been useful. For more tips related to saving money, check out these articles.