Life is all about balance. We’re rarely able to focus on just a single priority for very long. The area of personal finance is no exception. In this article, I’ll discuss how to pay off debt and save money at the same time without excessively diluting your efforts or jeopardizing your financial future.

How to pay off debt and save money at the same time (13 tips)

1. Budget your income carefully

To successfully save money while paying off debt, you need to allocate your resources wisely. In other words, make a budget! Here’s a simple approach I’d recommend.

Start by listing your monthly and yearly financial obligations, including minimum debt repayments and other essentials, such as groceries, rent, and utilities. The more comprehensive your list of expenses is, the better. If you really want to go the extra mile, read my article about unexpected expenses and incorporate any relevant ones as needed.

Next, plot your expenses out over the next 12 months. In other words, calculate how much you’ll spend on essentials over the next year.

Once you’ve done this, subtract the resulting number from your annual take-home pay.

You’ll be left with a figure representing the amount of money you have to allocate between saving, making more aggressive debt repayments, and any other discretionary financial moves.

The exact optimal percentage split between these categories will vary depending on your situation. Many of the subsequent tips in this article are designed to help you think critically about this.

However, the takeaway from this point should be the importance of allocating your discretionary income wisely. This is the essence of knowing how to pay off debt and save money at the same time. It’s how you’ll achieve the clarity needed to strategically balance repaying debt and saving.

2. Identify a clear purpose for saving

The strategy of saving while paying off debt involves using borrowed money as a tool for improving your financial situation. Unfortunately, many people who set out to do this end up spending the money frivolously instead of actually saving it.

It’s incredibly easy to fall into this trap if you don’t identify your purpose for saving. Ask yourself what the ability to save while paying off debt ultimately means to you. Will you be able to buy a house or retire sooner? Are you saving towards an emergency fund that will help you sleep better during turbulent times?

Identifying this purpose will help you derive as much benefit as possible in exchange for the greater amount of interest you’ll end up paying by keeping debt around longer.

3. Remember paying off debt can be an investment in itself

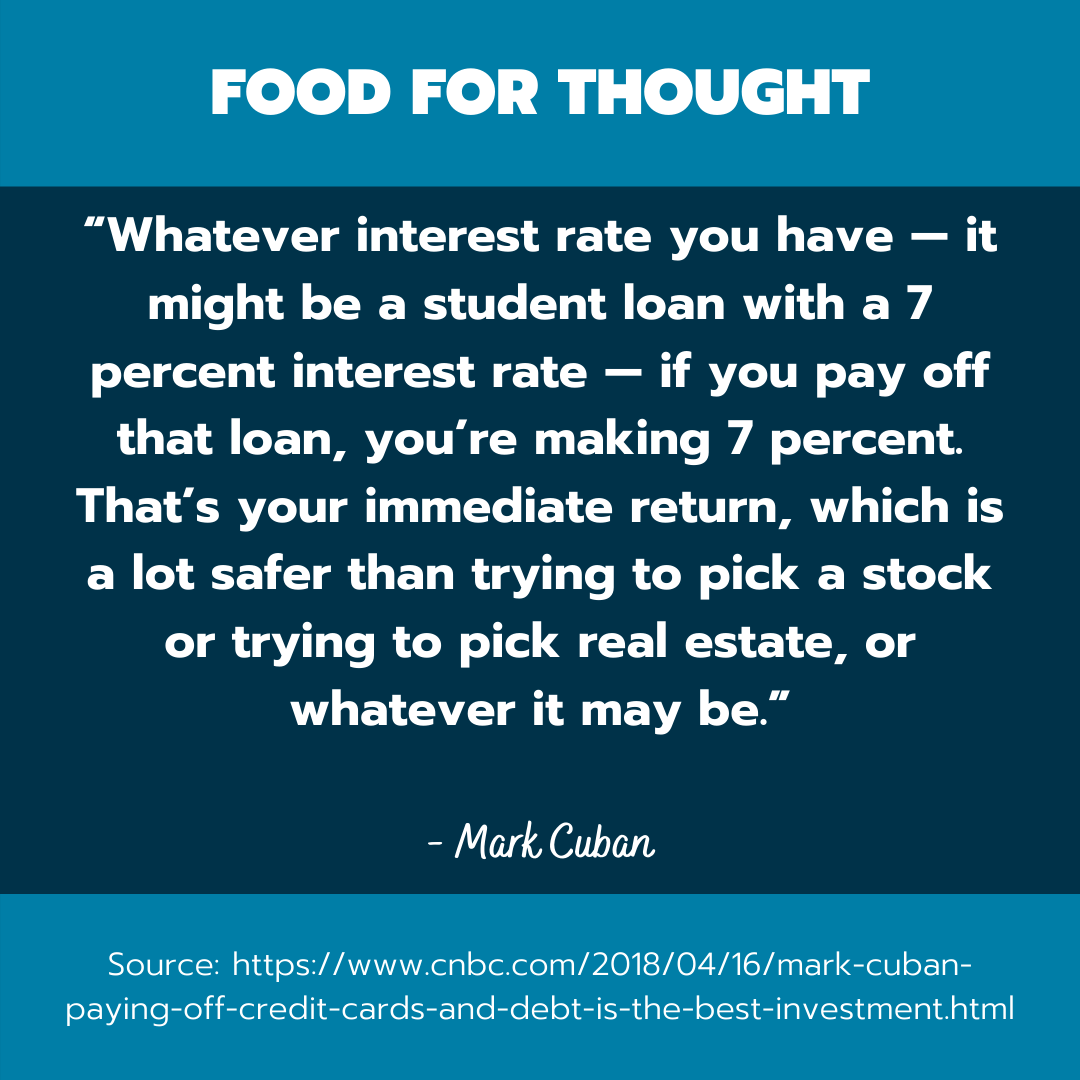

If your reason for saving while paying off debt is to generate a meaningful return on your money, consider this. Paying off debt can actually be a tremendous investment in and of itself, depending on your loan’s interest rate.

Here’s how it works.

Whenever you put money towards paying off debt, you immediately lock in a return equivalent to the amount of interest you would have paid by keeping the debt around.

On a credit card charging 14.58% interest, for example, any payment you make generates a 14.58% annual return because you’ve eliminated that much interest. No other investment on earth could produce this sort of immediate and guaranteed return.

Further, this return is completely tax-free. Whether you save $1,000 or $10,000 in interest, the government will not come after you for a slice of that economic benefit. It’s all yours.

This isn’t to say you shouldn’t save or invest while paying off debt. It’s just something to consider, especially if your motivation for passing on more aggressive debt repayments is to pursue more “exciting” benefits.

4. Not sure what to save for? Consider an emergency fund

If you still don’t have a specific reason for saving after reading the last two tips, here’s an idea: building an emergency fund if you don’t already have one.

Even when you have substantial debt, building an emergency fund can be a logical step towards financial stability.

After all, a financial emergency could very well eat up your income. If you previously put all of your extra cash towards aggressive debt repayments yet didn’t have an emergency fund, you’d be in hot water.

Even if you managed to eliminate your balance, you’d likely have to go back into debt for essential expenses. If you still had a balance, you’d be at risk of missing payments.

Experts generally recommend building an emergency fund large enough to cover three to six months of expenses. Even a more modest fund can go a long way towards mitigating the negative financial impact of an emergency, though.

Check out this article from Ashley at Common Cents Lifestyle for a few tips on assembling an emergency fund.

5. Figure out where your debt ranks in terms of priority

Not all debt is equal. Here’s the popular view among personal finance nerds regarding the level of urgency involved in eliminating various types of debt. According to this view, repayment becomes less urgent as you move down the chart.

| Type of debt | Typical interest rate | Priority level |

|---|---|---|

| Credit cards | 14.58% | 1 |

| Private student loans | 6.17% to 7.64% | 2 |

| Government student loans | 5.8% | 4 |

| Car loans | 5.27% | 3 |

| Mortgages | 2.88% | 5 |

The rationale behind this hierarchy is that it makes sense to get rid of high-interest debt promptly since compounding at higher rates significantly limits your ability to build wealth. In contrast, the financial consequences of keeping low-interest debt around are much lower.

What are the implications when it comes to saving while paying off debt?

Well, the benefits of saving always need to be contrasted against those of paying off your debt. High-interest loans arguably carry a greater burden when it comes to proving the benefits of saving rather than aggressively repaying debt.

For example, there’s little justification for saving money towards a vacation when you have $5,000 in credit card debt at an interest rate of 14.58%. In fact, you’re living beyond your means in this scenario. However, it’s less outlandish to save for something frivolous like a vacation when all you have is a mortgage at 2.88%.

After all, to tie this tip back to an earlier one, forgoing a 2.88% return on your money isn’t anywhere near as ludicrous as turning down a 14.58% one.

6. Consider saving in tax-advantaged accounts

The longer you keep debt around, the more interest you’ll ultimately pay. There’s no way around this, even if you decide the benefits of saving rather than repaying your loans more aggressively are worth it.

However, you may be able to offset the negative effects of this additional interest by saving within a tax-advantaged account, such as a 401k in the United States or RRSP in Canada.

Every dollar you deposit in these accounts reduces your taxable income for the year up to a certain limit. If you plan your contributions wisely with the help of a financial advisor, your tax savings can provide quite significant. They may even surpass your excess interest payments.

Tax-advantaged accounts exist for goals other than retirement, too. If you live in the United States, check out this article for a rundown.

7. Saving for a long-term goal? Consider investing

If your purpose for saving money while paying off debt involves a long-term goal like retirement or purchasing a home in 10 years, you may want to consider investing.

With the right strategy, investing can produce a much greater return over the long haul than you’d achieve by paying off low-interest debt.

Here’s what the math looks like.

Let’s say you have $600 and are deciding whether to keep it in a savings account or use it to pay off debt. In a savings account, the direct economic benefit during the first year would be 30 cents ($600 x 0.05%). If you put the $600 towards repaying a 5% interest loan, however, the economic benefit during the first year would be $30 ($600 x 5%).

If you’re using your savings to buy stocks, however, the results are very different. The U.S. stock market returns an average of 8% annually. Therefore, the potential economic benefit of saving and investing your $600 would be $48 ($600 x 8%) in the first year, which is greater than the $30 you’d gain using it to pay off debt.

This logic is why I’ve prioritized investing rather than making substantial extra payments towards my 1.09% car loan.

Now, investing is not right for everybody. Read this article to learn about the considerations you need to take when determining if you should throw money into the market. This article, meanwhile, offers valuable insights into the fundamental differences between saving and investing. It will help you figure out if this tip applies to your goals and financial situation.

8. Figure out how comfortable you are with debt

Figuring out how to pay off debt and save money at the same time is about more than just looking at raw numbers. Your emotions will also play a key role in determining the right approach.

For example, let’s say debt makes you feel uneasy. Whenever things seem rocky at work, your head gets filled with fears of losing your job and not being able to keep up with payments. When figuring out the ideal split between repaying debt aggressively and saving, you’d need to account for this.

Some people with this attitude towards debt prioritize eliminating even low-interest loans as quickly as possible. They want to be done with it.

Conversely, some people have no particular problem with debt and don’t mind making minimum payments while saving excess funds.

Think carefully about which category you fall into. Keep in mind, people commonly overestimate their financial risk tolerance. You may not be as calm and collected about investing rather than paying off debt when the market is in turmoil. Consider working with a financial advisor to get a more accurate picture of your risk tolerance.

9. Can’t keep up with debt payments or bills? Stop saving

Although it often makes sense to save while paying off debt, this doesn’t apply when you’ve fallen beyond on bills. Such a scenario represents a financial emergency during which pretty much everything other than catching up on bills loses priority.

This can be difficult to accept if you feel like you’re on a roll with your savings. However, you’ll do much greater damage to your financial situation by continuing to set money aside for purposes other than catching up on your expenses.

In other words, be practical, even if that means putting your plans to pay off debt and save money at the same time on hold.

10. Unlock more income

One challenge of saving and paying off debt at the same time is that you may feel demotivated by your apparent lack of progress with either goal. After all, no matter how you slice it, this approach splits your efforts.

If you feel stuck, consider earning more money. I know, I know – easier said than done. Or is it? I provide some concrete steps for boosting your income in this article.

By giving yourself more income to split between saving and paying off debt, you’ll move much faster towards both goals.

11. Stop accruing additional debt

One of the worst things you can do when trying to pay off debt is to rack up more of it at the same time. When you combine this behavior with the strategy of saving and paying off debt at the same time, it becomes particularly self-defeating since you’re ultimately not getting ahead.

If you find it hard to prevent yourself from tossing more expenses on credit, consider taking steps to limit your access. Some people cut their credit cards up and don’t order new ones until the balances have been eliminated. This may be particularly helpful if you have excessive amounts of credit card debt.

However you go about it, avoiding additional debt is crucial for making progress while paying off loans and saving at the same time.

12. Consider debt consolidation

Debt can be challenging enough to juggle on its own when you have multiple loans. When you throw saving into the mix, things can get overwhelming.

A debt consolidation loan can simplify the burden. It consists of a lump sum you can use to pay off multiple loans, leaving you with a single monthly payment. If your credit score or broader financial situation has improved since you initially acquired the debt, you may even be able to get a consolidation loan at a better interest rate.

Many financial institutions offer debt consolidation loans, including traditional banks and private lenders.

13. Automate what you can

Once you’ve identified the accounts in which you plan to save, consider automating deposits to them along with whatever loans you’re paying off. This is incredibly convenient since you won’t have to worry about transferring money manually every payday.

Automating your deposits also has the effect of removing your ability to make poor decisions about what happens with those funds. Your commitment to saving and paying off debt becomes as rigid as any of your other financial obligations. Before long, you won’t see progress towards your goals as being up for debate at all.

Conclusion

Saving money while paying off debt can be incredibly rewarding. I hope this article has been useful in communicating the steps you should take to ensure success. In summary, budget your income carefully and consider the many nuances involved in determining the appropriate split between debt payments and saving.

For more articles about personal finance, visit my blog here.